When you start earning above a certain threshold in the UK, your income falls into what many accountants call the “higher rate” tax band. This isn’t just a number on a payslip — it has real implications for tax planning, take-home pay and financial decisions. In this guide, we explain what the higher rate tax band actually is, why it exists, and smart strategies to reduce its impact.

What Is the Higher Rate Tax Band?

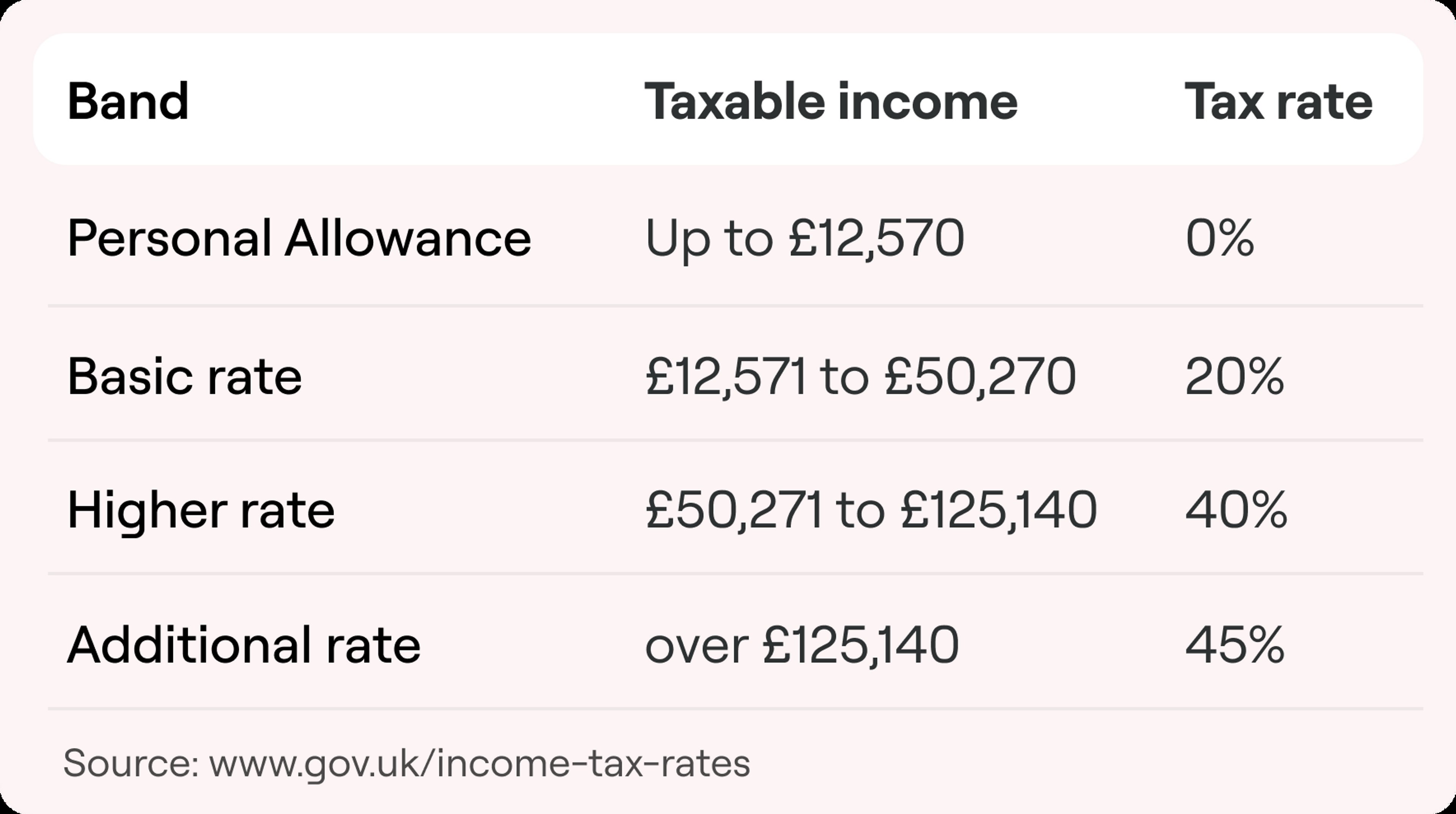

The UK personal tax system is progressive, meaning different chunks of your income are taxed at different rates. In simple terms for the 2025/26 tax year:

| Tax Band | Taxable Income | Tax Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

So when people refer to the 40% tax bracket, they are talking about income that falls between £50,271 and £125,140. Every £1 you earn in this band is taxed at 40p in the pound.

Does the Higher Rate Apply to All Income Types?

Not all income is treated the same — and this is where smart planning can reduce your tax bill.

- Employment Income & Director Salaries: Taxed at 20%, 40% or 45% depending on total income.

- Dividends: Have their own tax bands (8.75% basic, 33.75% higher, 39.35% additional). This means a director taking dividends instead of salary could pay less tax.

- Rental Income & Interest: Count towards taxable income and can push you into the 40% bracket.

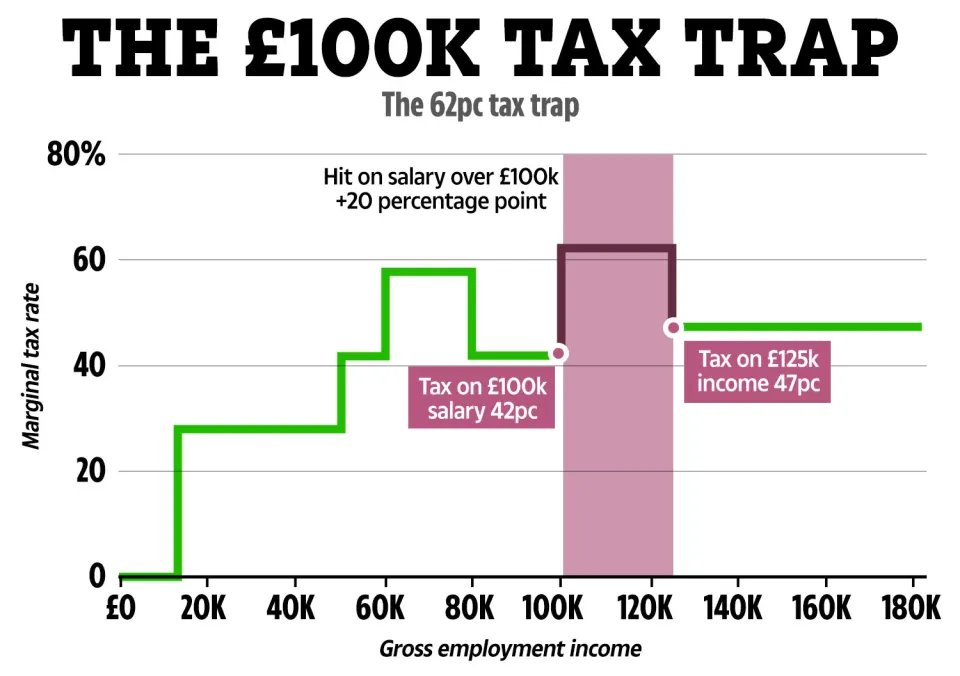

The "60% Tax Trap": Earning Over £100,000

There’s a tax quirk higher earners need to watch: For every £2 you earn over £100,000, you lose £1 of your personal allowance.

By the time your income reaches £125,140, your full £12,570 personal allowance is gone. The effective marginal rate in this “withdrawal zone” can be as high as 60%. Suddenly earning an extra £1 can cost you 60p in tax and lost allowance.

Effective Strategies to Reduce Higher Rate Exposure

While you can’t avoid tax, there are legal, HMRC-compliant strategies to reduce your exposure to the 40% rate:

- Use Tax-Efficient Compensation Structures: Directors can balance salary, employer pension contributions, and dividends to reduce overall tax.

- Maximise Pension Contributions: Pension contributions attract tax relief at your marginal rate — worth up to 40% (or even 45%) for higher earners.

- Utilise ISA Allowances: Interest, dividends or gains inside an ISA are tax-free.

- Claim Legitimate Business Deductions: Valid business expenses reduce taxable income.

- Consider Spreading Income: Defer bonuses or spread dividend payments to avoid spiking into a higher band.

What Happens If You Accidentally Cross the Threshold?

If your total income exceeds £50,270, you will automatically pay 40% on the excess. This is calculated in your Self Assessment, but it’s easy to underestimate if you have multiple income streams. Accurate forecasting is essential.

Conclusion: Understand It, Plan It, Don’t Fear It

The higher rate tax band is simply part of the UK’s progressive system. For many directors and business owners, it's predictable and manageable with planning. But ignoring it costs real money.

Want a Personal Tax Review? If you’re a high earner or director and want to optimise your tax position, email us at [email protected] for a tailored consultation.

Need Expert Advice?

Our team can help you navigate these changes and ensure your business remains compliant and tax-efficient.

Recent Articles

Moving to India Permanently While Keeping UK Property: A Complete UK–India Tax Planning Guide

January 28, 2026

HMRC Enquiries Into CIS Subcontractors: Why Inflated Expenses Trigger Investigations (And How to Protect Yourself)

January 25, 2026