For long-term UK residents who plan to move to India “for good”, the tax position does not simply stop at the border. UK property, historic residence, and ongoing income streams mean that UK tax obligations continue, while Indian tax exposure begins.

This creates a classic cross-border planning scenario where mistakes can lead to unexpected UK tax bills, double taxation, capital gains surprises, and long-term inheritance tax exposure.

1. The Typical Scenario We See

A common profile looks like this:

- UK resident for 15+ years, British citizen

- Two UK rental properties (one mortgage-free, one with a mortgage)

- Currently UK resident with employment + rental income

- Planning to move to India permanently in April 2026

- Will visit the UK a few times a year to see family

This creates a “UK leaver with retained assets” profile. The main planning areas are UK tax residence status, UK tax on rental income, Capital Gains Tax, Indian tax relief, and Inheritance Tax (IHT).

2. UK Tax Residence After Leaving

After departure, UK tax residence is determined under the Statutory Residence Test (SRT). This looks at the number of days spent in the UK and your UK “ties” (family, accommodation, work, etc.).

If visits are limited to short family trips and there is no UK work or excessive UK presence, many individuals can successfully become non-UK resident. However, retaining access to a UK home or spending extended periods in the UK can risk re-triggering UK residence.

👉 This is one of the most common areas where people accidentally fail — professional modelling is essential.

3. UK Tax on Rental Income After Becoming Non-Resident

Becoming non-resident does not remove UK tax on UK property. Income from UK-situated property remains taxable in the UK regardless of where you live.

The Non-Resident Landlord (NRL) Scheme

Once non-resident, landlords normally fall within HMRC’s Non-Resident Landlord Scheme. Letting agents may be required to deduct basic-rate tax from rents unless you apply to receive rent gross and settle tax via Self Assessment. Applying early avoids unnecessary cash-flow issues.

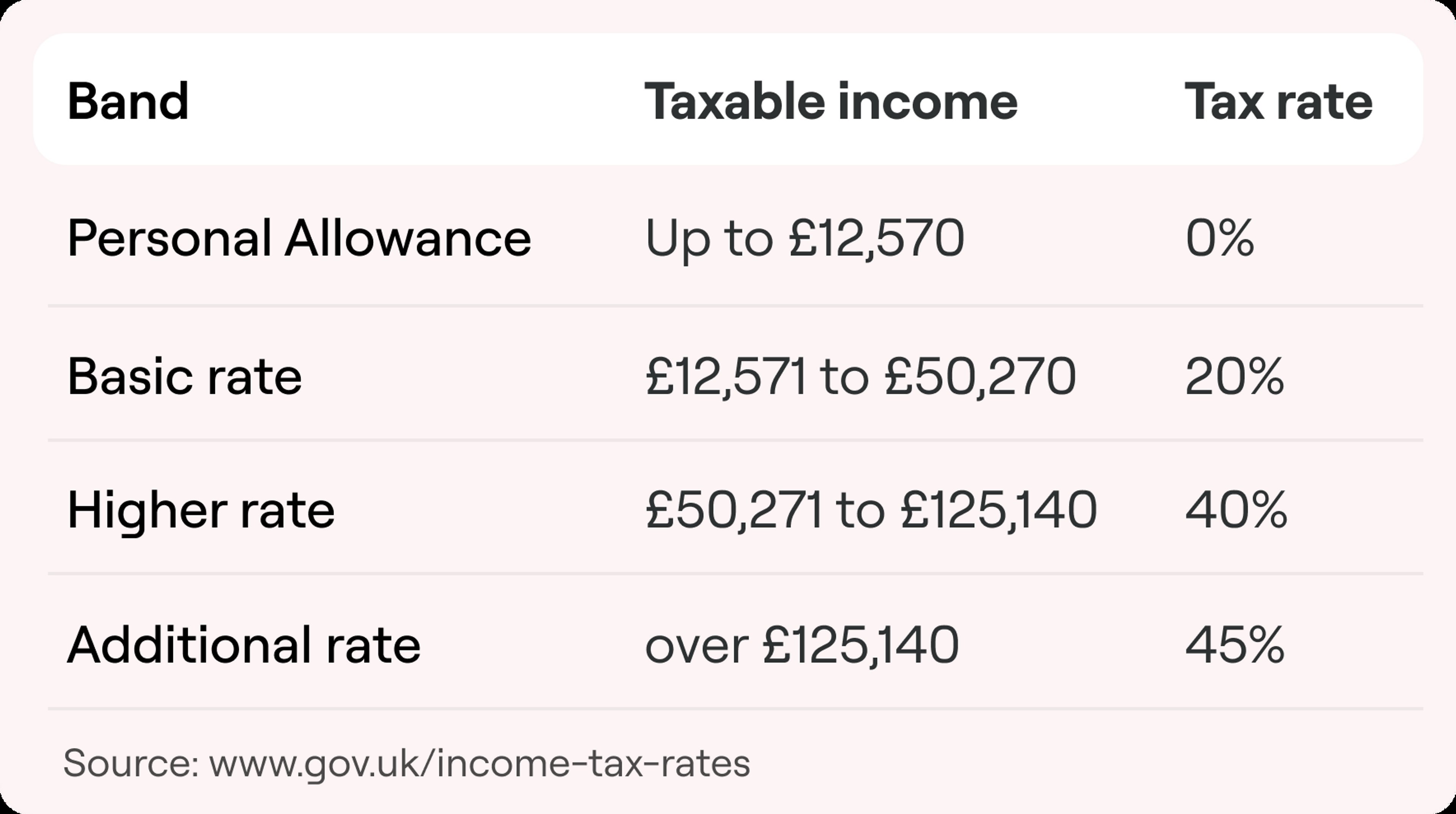

4. Personal Allowance and UK Tax Bands

Non-residence does not automatically remove entitlement to the UK personal allowance. British citizens generally continue to qualify for the UK personal allowance and can still use standard UK tax bands on UK-source income.

This means rental profits may still benefit from the personal allowance and the basic-rate band before higher rates apply. Importantly, UK tax applies only to UK-source income; foreign income is generally not taxable in the UK once non-resident.

5. Capital Gains Tax on Selling UK Property

Non-residents are fully within scope of UK Capital Gains Tax on UK land and property. Gains must be reported via the UK property CGT system, usually within strict time limits.

Planning Opportunity: Before leaving, it is worth comparing selling while UK resident vs. selling after becoming non-resident. Factors include UK CGT rates, Indian capital gains tax treatment, and double tax relief under the UK–India treaty.

6. Indian Tax and the UK–India Double Tax Treaty

Once settled in India, individuals often become Indian tax resident, meaning India taxes worldwide income, including UK rents. However, the UK–India Double Taxation Agreement allocates taxing rights: UK generally has primary taxing rights over UK property income, and India usually provides credit relief for UK tax paid.

👉 UK and Indian tax advice should be aligned — fragmented advice often leads to over-taxation.

7. Inheritance Tax (IHT): The Long-Term Risk

Many long-term UK residents remain exposed to UK Inheritance Tax even after leaving. UK IHT increasingly focuses on long-term UK residence, not just domicile. UK-situated assets (including UK property) remain within the UK IHT net.

Planning may include reviewing ownership structures, gifting strategies, life insurance, and coordinating UK and Indian succession rules.

8. UK Self Assessment and Compliance After Departure

The year of departure is critical. A final UK resident Self Assessment return is normally required, and split-year treatment may apply. After becoming non-resident, UK Self Assessment usually continues for UK rental income only.

9. What Should Be Done Before April 2026?

Before leaving, it is sensible to:

- Confirm non-residence under the Statutory Residence Test

- Review whether to retain or sell UK properties

- Obtain valuations for future CGT planning

- Register for the Non-Resident Landlord Scheme

- Notify HMRC of address and status changes

- Coordinate with Indian tax advisers

- Review wills, estate planning, and IHT exposure

How Mayfair Tax Advisors Can Help

This is a high-risk cross-border tax scenario where joined-up advice is essential. We can model UK residence outcomes, advise on non-resident landlord tax, manage Self Assessment compliance, and plan CGT strategy.

Leaving the UK does not end UK tax — it changes it. Handled correctly, this transition can be efficient and compliant.

Need Expert Advice?

Our team can help you navigate these changes and ensure your business remains compliant and tax-efficient.

Recent Articles

HMRC Enquiries Into CIS Subcontractors: Why Inflated Expenses Trigger Investigations (And How to Protect Yourself)

January 25, 2026

The Personal Allowance Taper & £100k Tax Trap: Why Your Tax Bill Jumps After £100,000

January 24, 2026