For many directors, senior employees, and high earners, crossing the £100,000 annual income threshold comes as a shock. It’s not just about paying 40% tax Read our guide on the Higher Rate Tax Band. — it’s about the Personal Allowance Taper, a mechanism that can create an effective marginal tax rate of over 60%. This article explains how the trap works, why your tax code might be under-collecting tax, and what you can do about it.

What Is the Personal Allowance?

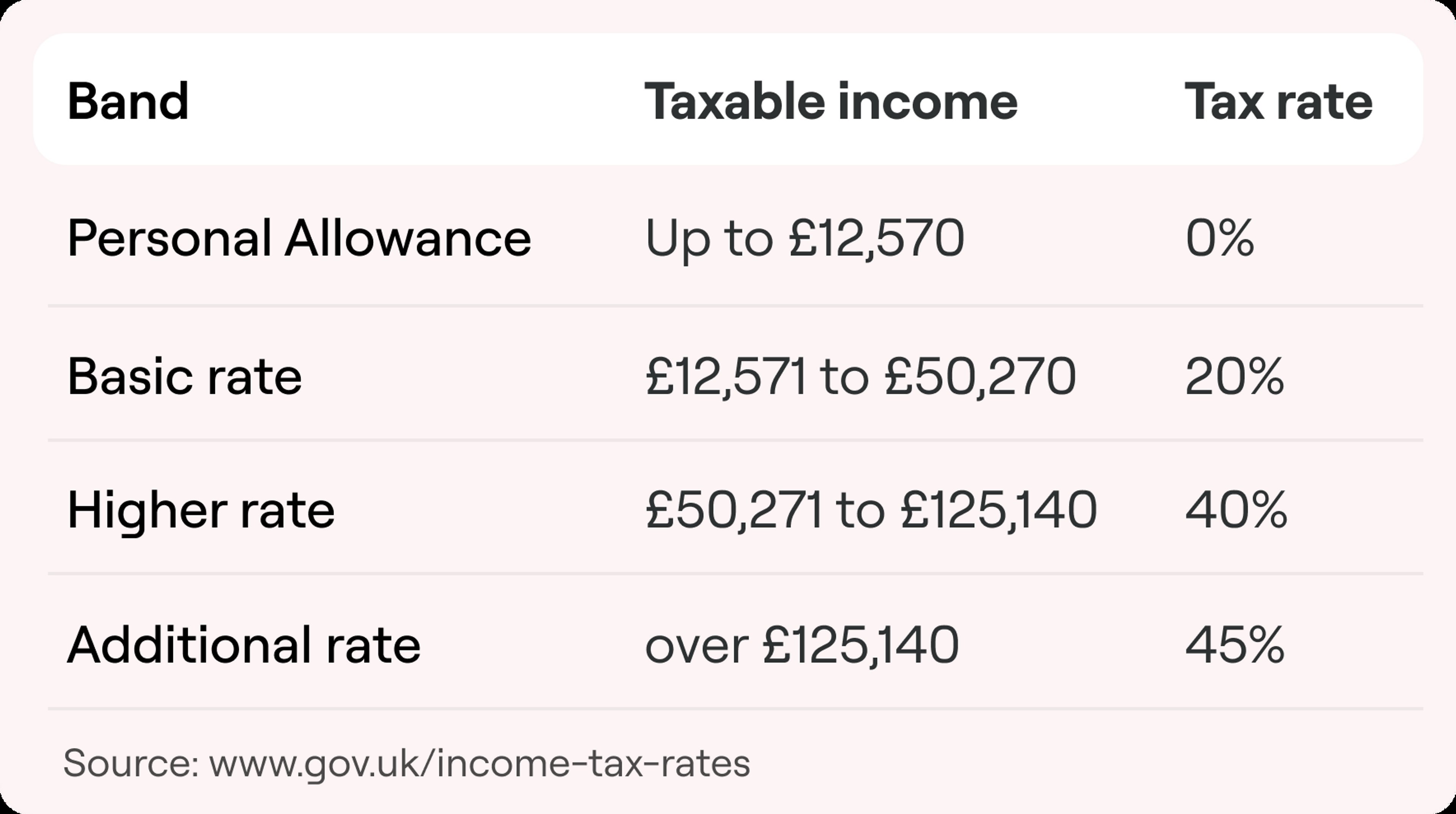

For the 2025/26 tax year, the standard Personal Allowance is £12,570. This is the amount of income you can earn tax-free. It applies to salary, self-employment profits, rental income, and pensions.

What Happens When You Earn More Than £100,000?

Once your Adjusted Net Income exceeds £100,000, your Personal Allowance is gradually withdrawn. The rule is simple:

For every £2 of income above £100,000, £1 of your Personal Allowance is lost.

This continues until your income reaches £125,140, at which point your Personal Allowance is zero.

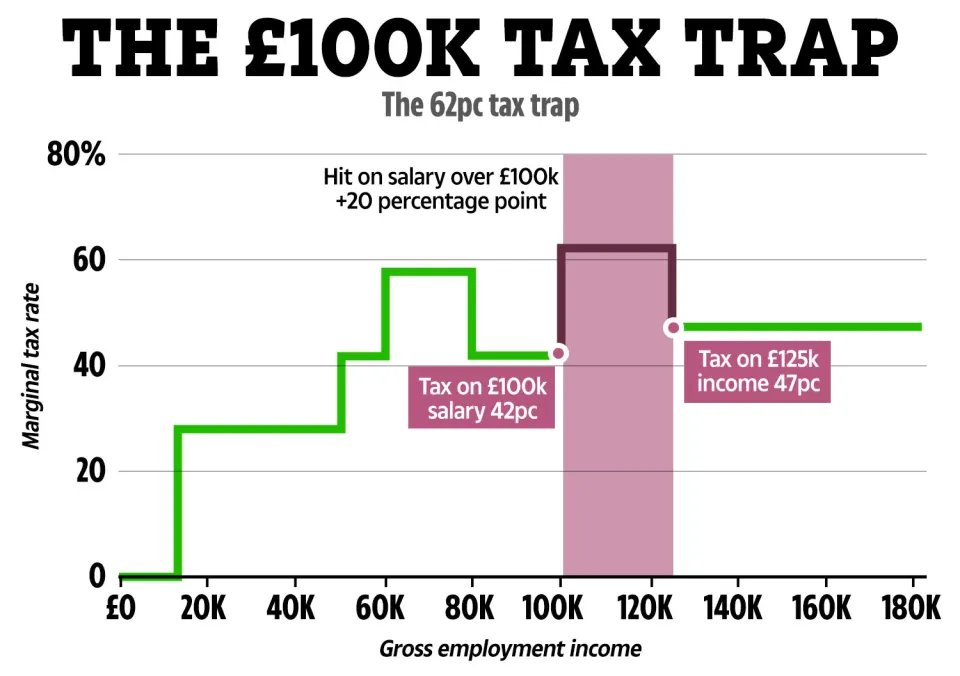

Why This Creates the ‘60% Tax Trap’

Between £100,000 and £125,140, you are hit with a double whammy:

- You pay 40% tax on the extra income.

- You lose tax-free allowance, meaning more of your existing income becomes taxable at 40%.

The Math: For every £100 you earn in this band, you pay £40 in tax directly. But you also lose £50 of allowance, which adds another £20 of tax. Total tax = £60. That is an effective marginal rate of 60%.

Why Your Tax Code Might Be Wrong

HMRC’s PAYE system often fails to catch this in real-time. If your tax code (e.g., 1257L) isn't adjusted during the year to reflect the taper, you will underpay tax month-by-month. This leads to a nasty surprise: a P800 tax calculation or Self Assessment bill after the tax year ends.

How Freezing Tax Thresholds Makes This Worse

With tax thresholds frozen, "fiscal drag" is pulling more people into this trap simply through inflation-linked pay rises. It’s a stealth tax increase that affects thousands of additional taxpayers every year.

Ways Directors & High Earners Can Manage This

While you must pay what you owe, you can manage your Adjusted Net Income to keep your allowance:

- Increase Pension Contributions: Personal pension contributions reduce your adjusted net income. A £5,000 contribution could save you £3,000 in tax (60% relief).

- Salary Sacrifice: Exchange salary for non-cash benefits like electric cars or additional pension, which are taxed more favourably.

- Charitable Donations: Gift Aid donations also reduce your adjusted net income.

- Defer Income: If you control your own company, consider delaying dividends or bonuses to a tax year where your income is lower.

Frequently Asked Questions (FAQs)

Does pension contribution reduce adjusted net income? ▼

Yes, personal pension contributions are one of the most effective ways to reduce your adjusted net income and regain your Personal Allowance.

What is the 60% tax trap? ▼

It refers to the effective marginal tax rate of 60% on income between £100,000 and £125,140 due to the tapering of the Personal Allowance.

Official Government References

For detailed guidance, verify these rules on GOV.UK:

When You Should Seek Professional Support

If you are a director with variable income, or a high earner facing an unexpected tax bill, professional planning is essential. At Mayfair Tax Advisors, we can forecast your liability, check your tax codes, and help you structure your income efficiently.

Don't get caught by the 60% trap. Email us at [email protected] for a personal tax review.

Need Expert Advice?

Our team can help you navigate these changes and ensure your business remains compliant and tax-efficient.

Recent Articles

Moving to India Permanently While Keeping UK Property: A Complete UK–India Tax Planning Guide

January 28, 2026

HMRC Enquiries Into CIS Subcontractors: Why Inflated Expenses Trigger Investigations (And How to Protect Yourself)

January 25, 2026